Strategic Budgeting Resources

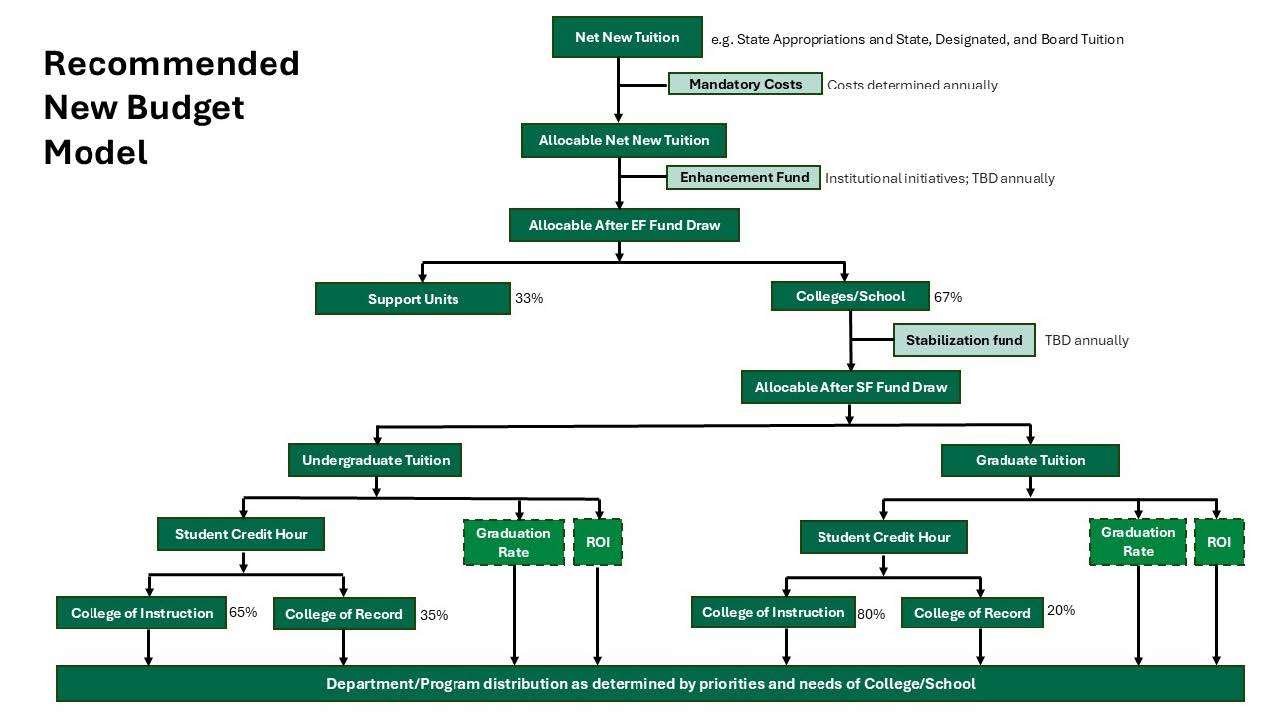

New budget model and annual process

This comprehensive report offers a review of the aims, scope of activity, and recommendations the Strategic Budget Steering Committee made in creating a new budget model and annual process. The model focuses on net new monies while allowing for strategic use of reserves, when possible, to support important and prioritized initiatives. This report introduces the specifics of the budget model, updated processes, and reasons for the proposed changes.

Download a summary of the report

This list has been alphabetized to help you more easily located the terms and their definitions. Click on the letter below to expand the box and list all of the terms that begin with that letter.

A

Academic Units: Primarily the schools and colleges; entities whose primary mission is teaching or teaching and research.

Activities-based: A budgeting model that awards financial resources to institutional activities that see the greatest return, in the form of increased revenues, for the institution in a defined period

Administrative Units: Units that provide support and operational services for all other units within the university (i.e., Human Resources, Facilities, Office of the President, Office of the Provost, etc.).

Allocation: A method of distributing budgeted costs and revenues to applicable units.

Auxiliary Units: units that operate almost as a stand-alone business; revenue and expense stay within the units to support operations, maintenance of buildings, etc. Examples include housing, dining, University Union, parking/transportation, etc.

B

Base Budget: the total source of funds and total use of funds that are received and distributed on an annual and recurring basis. The total use of funds is primarily for unit operations, campus wide expenditures, and state university grant distributions.

Board of Regents (BOR): An appointed body by the Governor of Texas who has general supervision and fiduciary responsibilities over the welfare and conduct of the University of North Texas.

Budget Authority: Annual resource allocation to each management unit; ability to spend.

Budget Cycle: The regular process of preparing, approving, and executing the budget, typically annually.

Budget hearings: scheduled meetings between college deans and provost office to discuss budgetary deficits, surpluses, needs and special funding requests.

Budget Model: how an institution organizes their costs and revenues, including allocations, cost/revenue sharing, overhead, etc. Common models for higher education include:

Budget Modeling Principles: The established guidelines used to govern the creation and management UNT’s budgeting model and strategy. These principles were created by the Strategic Budget Transformation Steering Committee in Fall 2024 to ensure that the new budget reflected key institutional goals.

C

Capital Budget: A plan for long-term investments in fixed assets like buildings, machinery, and equipment.

Carry Forward: Budget authority or residual fund balances that roll to new fiscal year.

Central Administration: Operational and administrative services provided by the University to all academic, administrative, and auxiliary units that allow for the overall functioning of the Institute toward the achievement of its mission and goals.

Centralized: A budget model aimed at creating a central pool of revenue, made up of tuition revenue from all colleges or programs, state funding, and ancillary streams of revenue. This budgeting practice delegates decision-making powers to upper-level administration, who distribute funds to subsidiary units. Typically, colleges and universities combine aspects of centralized budgeting with decentralized budgeting.

Contingency Fund: A reserve set aside for unexpected expenses or emergencies.

D

Debt Service: The cash that is required to cover the repayment of interest and principal on a debt for a particular period.

Differential Tuition: tuition charged for each specific university student based on the College or Program providing the course.

Direct Revenues: Revenues generated from activities of the academic units outside of tuition and state appropriations, such as contracts or partnerships.

E

Endowment Distributions: The portion of all endowment earning’s that become available for spending or resource allocations.

Exemption: mechanism used to exempt students from charges for portion or all of tuition and fees. Common examples include: Hazlewood; Adoption; Deaf/Blind; Orphan; Peace Officers; Firefighter; Nurse

Expense: Transaction representing outflow of funds to employees, suppliers, and other parties to support university activities.

F

Facilities and Administration Costs (F&A): These are costs that are incurred for common or joint objectives and therefore cannot be identified readily and specifically with a sponsored project, an instructional activity, or any other institutional activity.

Fees: charged to defer costs related to maintaining and operating specific facilities, providing services and consumable supplies, etc.

Fiscal Year: The 12-month period in which the UNT budget is in place. The fiscal year for Texas higher education is Sept. 1 through Aug. 31.

Formula funding: A method for distributing state funds to higher education institutions, including UNT, in an equitable manner. The Higher Education Coordinating Board (THECB) calculates the formula and presents its recommendations to the Legislative Budget Board in June of even-numbered years.

G

Grants & Contracts: aka Sponsored Projects; Programs and projects financed by federal and non-federal agencies and organizations which involve performance of agreed upon work and deliverables, often research related.

H

Hold Harmless: Policy of guaranteeing that unit budgets will be made whole during a new budget model implementation. Hold harmless policies minimize risk to units as leadership reviews and refines a model and gives unit leaders time to learn how a model works before fully living with it.

I

Incremental: A traditional budget model in which budget proposals and allocations are based on previous year’s funding levels. Only new revenue is allocated. Budget cuts are made as a percentage of the institution’s historical budget and are typically across-the-board in reach.

Indirect Cost Recovery (IDC) - also known as Facilities and Administration Costs (F&A):

Those costs associated with the conduct of sponsored projects that are incurred for

common or joint objectives and therefore are not readily identifiable with a specific

project. These costs are legitimate costs incurred by the University in support of

the performance of sponsored projects. Costs include items such as building maintenance,

utilities/electricity, office supplies, telephone charges, etc. F&A rates are the

mechanism used to reimburse the University for these infrastructure costs associated

with sponsored projects. F&A rates are assessed as a percentage of the direct costs

of the sponsored projects. These are actual costs to the University and support sponsored

projects being performed by the University. UNT allocation plans are shown in tables

below:

Standard F&A Distribution

| College/Dept/PI | VP Research | VP Finance | Total |

| 32.5% | 37.5% | 30% | 100% |

Standard College/Dept/PI Distribution

|

College

|

College %

|

Deptartment % | PI % |

| College of Engineering | 12.5 | 10 | 10 |

| College of Liberal Arts & Social Sciences | 10 | 12.5 | 10 |

| College of Merchandising, Hospitality & Tourism | 10 | 12.5 | 10 |

| College of Business | 10 | 12.5 | 10 |

| College of Education | 10 | 12.5 | 10 |

| College of Information | 10 | 12.5 | 10 |

| College of Science | 10 | 12.5 | 10 |

| College of Visual Arts & Design | 10 | 12.5 | 10 |

| College of Health & Public Service | 11.25 | 11.25 | 10 |

| College of Music | 10 | 12.5 | 10 |

| UNT Libraries | 22.5 | 0 | 10 |

Instructional Fees: vary by course and fall into either Academic Fees or Laboratory fees.

-

Academic fees are assessed at the college/school level based on the estimated costs of goods and services related to instruction. Funds can be used to cover consumable supplies, syllabi, tests, classroom guest lecturers, salaries/wages of employees who assist in the preparation, distribution, and supply of classroom materials and some equipment purchases related directly to student participation in the classroom.

-

Laboratory fees are only applicable to courses which require students to register for a laboratory section. Laboratory fees are collected to cover the cost of materials and supplies used by students in the laboratory.

M

Mandatory Fees: assessed for university-related services available to students. Student Service, Athletics, Rec Ctr, Environmental Services, Student Union, Medical Services, Transportation, International Education, Learning Support, Internation Student, Master’s Advising Fee.

O

Out-of-State Teaching Fees (OSTF): Non-resident students living outside of Texas while taking UNT courses are charged an Out-of-State Teaching Fee in lieu of tuition and instructional fees. This fee must cover the cost of instruction and is set by each academic department annually.

P

Performance-based: A model that awards funds based on defined outcomes and standards, rather than just the revenue potential alone. An effective performance budget will highlight how well dollars fund day-to-day functions and provide predictors on how likely certain functions and programs are to produce positive outcomes.

Program Fees: fees assessed to help with costs for specific programs. Examples include Coursera BAAS, Advanced Data Analytics, Audiology & Speech, College of Business Master’s, College of Education Educator Prep, College of Information PhD Learning Technology, & Honors College.

Q

Quasi/Semi-restricted funds: funds that have a defined scope for control and/or expenditure.

R

Revenue: Inflow of funds from ongoing operations (ex: Tuition and Fees).

Responsibility Center Management (RCM): Is a budgeting model under which revenue-generating units are wholly responsible for managing their own revenues and expenditures. This model is seen as a decentralized method of managing an organization’s budget. Operational authority is delegated to schools, divisions, and other units within an institution, allowing them to prioritize their academic missions. Each unit receives its own revenues and income, including the tuition of its enrolled students. In this way, units effectively compete for students. Each unit is also assigned a portion of government support (where applicable). However, units are also responsible for their own expenses, as well as for a portion of expenses incurred by the college or university’s general operations.

Reserves: Accumulated resources from prior financial transactions which provide flexibility for the central institute and units to cover unanticipated expenses and enable leaders to invest in and grow the institution.

Restricted Funds: Funding that is limited to a specific use e.g. sponsored funds and some fees.

S

Sales of Goods Sold: direct sales of services and goods produced by university units.

State Appropriations: Funding provided by the state to colleges and universities. These funds can be unrestricted (used for any purpose) or restricted (limited to a specific use).

Semester Credit Hours (SCH): the total number of credit hours in which a student is enrolled or has successfully completed during a semester term. The credit hour is a unit of measurement for the amount of instructional and learning time required to meet the student learning objectives of a university-level course.

Shadow budget: a fiscal model exercise commonly used to assess financial hypotheses and behavior accuracy of a budgeting model.

Sponsored Projects: Programs and projects financed by federal and non-federal agencies and organizations which involve performance of agreed upon work and deliverables, often research related.

T

Tuition: when we talk about tuition, we typically mean Board Designated tuition, but it is not the only source of tuition dollars.

- Statutory Tuition: authorized under Texas Education Code § 54.051 for undergraduate students and is a mandatory amount set by the state.

- Board Authorized Tuition: authorized under Texas Education Code § 54.008 for graduate programs and the rate is set by the Board of Regents. Texas Education Code § 54.008 authorizes institutions to set tuition at rates not more than twice that of undergraduate tuition.

- Designated Tuition: authorized under Texas Education Code § 54.0513 for undergraduate and graduate students and is set by the Board of Regents. It is the amount the Board of Regents considers necessary for the effective operation of the institution. Rates vary between undergraduate and graduate students.

U

Unrestricted Funds: Resources that are not limited to a specific use (e.g. Foundation funds).

W

Waiver: mechanism used to waive out-of-state tuition rates, so a student is charged in-state rates instead.

Z

Zero-based: A budgeting method that clears the previous budget every year and each institutional unit reapplies for funding. This means that units or departments must continually justify their funding requests year over year.